;

;

U.S. Market Profile

full report (PDF)

(Date of Publication: October 11, 2024)

This Global Market Profile report contains two sections. The Market Landscape section offers a look at spending forecasts for California. The Audience Insights section includes data on travel behaviors and accommodation and booking preferences.

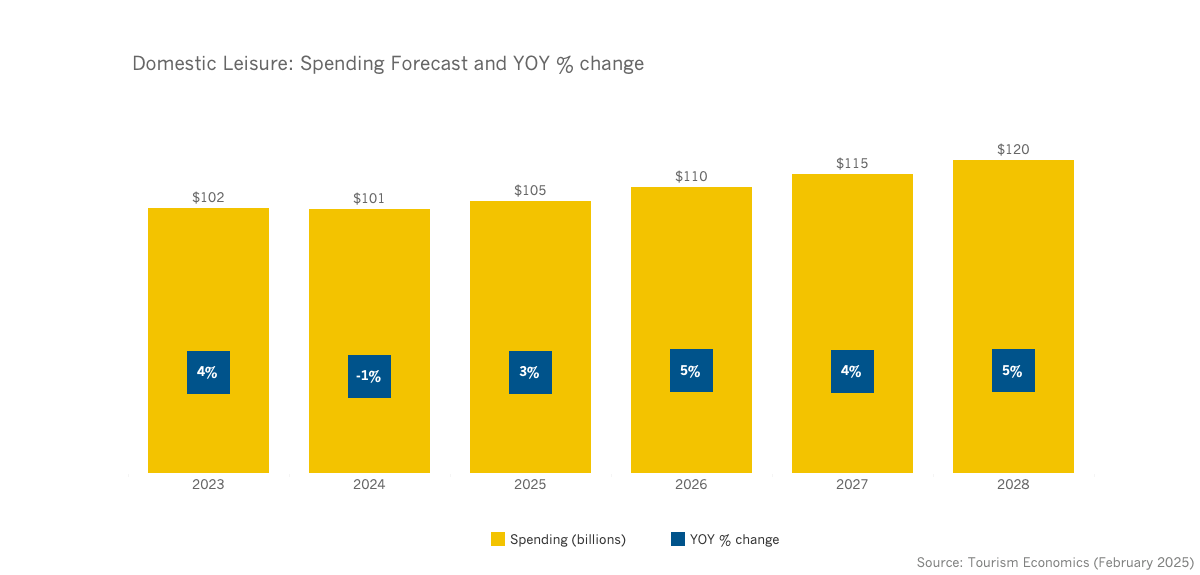

MARKET LANDSCAPE

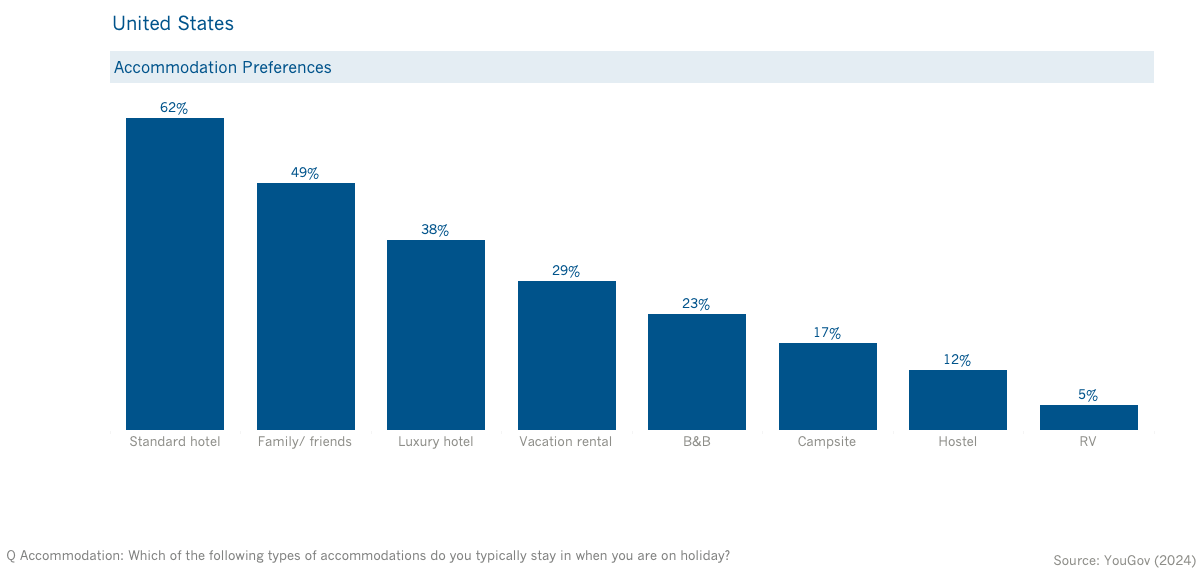

AUDIENCE INSIGHTS

Related Research